As a new calendar year begins, Fit and Proper reviews once again come into focus across Regulated Financial Institutions. Annual declarations, internal reviews and board attestations are familiar fixtures of the compliance cycle. These remain a key mechanism through which Regulated Financial Institutions demonstrate to the Monetary Authority of Singapore (MAS) that individuals performing regulated roles continue to meet suitability expectations.

The MAS’ Guidelines on Fit and Proper Criteria (FSG-G01) (the Guidelines) make clear that Fit and Proper is not designed to be a yearly administrative ritual. It is an ongoing assessment that must be applied proportionately, thoughtfully and with proper documentation. It is a core governance safeguard, one that underpins trust in the financial system and the people who operate within it.

As Regulated Financial Institutions prepare for 2026 governance, compliance and declaration cycles, this is an appropriate moment to revisit what Fit and Proper truly means in practice.

The MAS Fit and Proper Framework

Trust forms the fundamental basis for an effective and efficient financial services market.

Clients place their savings, investments and long-term financial plans in the hands of institutions and professionals on the premise and expectation that these parties are competent, ethical and act in accordance to their fiduciary duties in the Client’s best interests. Regulators, in turn, need confidence that such entities are led and staffed by individuals who meet those same standards and can be trusted to make competent, sound decisions.

This is where the Fit and Proper standards play a central role towards safeguarding the interests of the end consumer, and of the hiring Regulated Financial Institution.

While the MAS has set the professional and ethical expectations for those who operate within Singapore’s financial system, it is the operators that are responsible for seeing out such expectations in their initial and ongoing hiring and compliance policies and processes. The objective is not only to address misconduct when it occurs, but to establish a clear baseline of suitability, competence and integrity for those performing regulated roles, thereby reducing the risk of misconduct and governance failures over time.

The Guidelines on Fit and Proper Criteria (FSG-G01)

The Guidelines apply broadly across the multitude of regulated activities here in Singapore. This includes the Capital Markets, Financial Advisory, Insurance and Payment Services sectors, as well as entities separately regulated under the Financial Services and Markets Act.

There is the expectation that every relevant person is to satisfy the Fit and Proper standards set out in the Guidelines. At the same time, MAS also recognises that different roles carry different responsibilities and accordingly requires subjective assessments to be calibrated to the nature, scope and risk profile of the role in question.

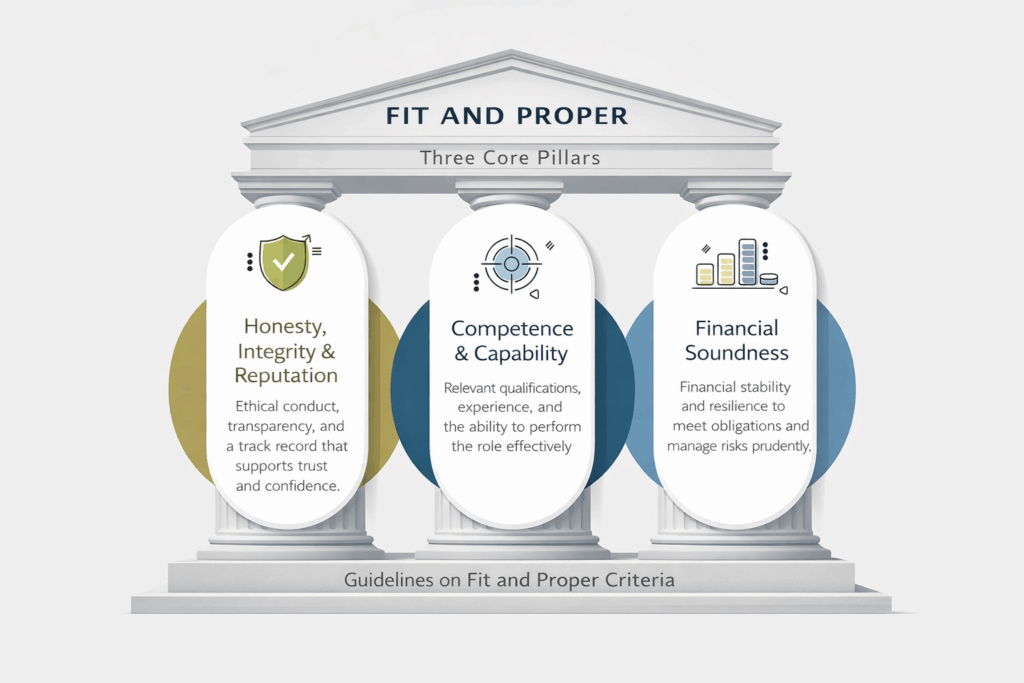

The Guidelines are built on three core pillars:

1. Honesty, integrity and reputation – The individual must be of good character and conduct themselves with integrity

2. Competence and capability – The individual must possess the qualifications, skills and experience necessary for their role

3. Financial soundness – The individual must manage their financial affairs prudently

These pillars apply consistently across sectors, although the depth and manner of assessment will vary depending on the role and its associated risks. On paper, the framework is simple. In practice, it requires a more nuanced evaluation that requires detailed deliberation.

Who Is Subject to Fit and Proper Assessments

The Guidelines and their applicability do not stop at the boardroom door.

The requirements extend well beyond just board members and chief executives. Under the Guidelines, they apply to a wide range of individuals, including:

- CEOs, directors, controllers and senior management

- representatives and other regulated individuals

- employees and officers of payment service providers

- staff of capital markets intermediaries

- individuals involved in digital token service providers

In other words, if a role can affect clients, markets or the handling of monies, it will be in scope.

This wide application addresses potential risk of certain functions extending beyond leadership roles to anyone whose decisions, systems, or customer interactions can affect market integrity, customer interests, or institutional soundness.

For Regulated Financial Institutions, this means Fit and Proper implementation and monitoring frameworks must be practical yet comprehensive enough to apply across the organisation, not just at senior levels.

Fit and Proper in Practice: Beyond a Tick-Box Exercise

Contextual and Proportionate Assessments

One of the most frequently misunderstood aspects of the Guidelines is how past conduct is treated.

The Guidelines are explicit that failing to meet one criterion does not automatically result in refusal, revocation or regulatory action. Regulated Financial Institutions are expected to consider factors such as the seriousness of the issue, its relevance to the role and the time that has passed as part of their assessment.

This position was reinforced in the MAS’ Parliamentary Reply on Fit and Proper assessments and career entry. MAS clarified that past conduct, including matters raised publicly, does not in itself render an individual unfit for a career in the financial services industry. What matters is whether, once viewed in context to the individuals’ role and function, the individual is suitable to perform the specific role responsibly and competently.

For compliance teams, this underscores the importance of reasoned decision-making supported by documentation, rather than rigid or formulaic assessments.

Implications for Hiring, Onboarding and Role Changes

Fit and Proper considerations arise at multiple points in an individual’s lifecycle within a Regulated Financial Institution These include initial hiring, onboarding into regulated roles, promotions, changes in responsibilities and transitions across business lines.

While Human Resources (HR) teams often lead recruitment processes, compliance oversight plays a critical role in ensuring that Fit and Proper assessments are conducted consistently and aligned with regulatory expectations. Clear communication between HR, line management and compliance is essential to ensure that assessments are conducted consistently and aligned with regulatory expectations.

For Singapore Fund Management Companies, the Guidelines on Licensing and Conduct of Business for Fund Management Companies (SFA 04-G05) also set out specific expectations on the conduct of background and due diligence checks as part of the Fit and Proper assessments. Paragraph 3.6 of SFA04-G05 states that Singapore Fund Management Companies should perform adequate due diligence on prospective representatives and employees, including reference checks with previous employers to verify credentials, work experience and any disciplinary record. Where individuals are hired based on an asserted investment track record or strategy, such entities are also expected to validate such track records before appointment, rather than relying solely on representations made by the individual.

These expectations underscore the importance of close coordination between HR, senior management and compliance functions. Without a clear process, ownership and communication, Fit and Proper assessments risk becoming fragmented or inconsistently applied.

From a governance perspective, Fit and Proper requirements are best integrated into these processes early, rather than introduced at the end as a final hurdle.

Fit and Proper Declarations and Ongoing Obligations

Declarations as Part of Regulatory and Internal Governance

In practice, Fit and Proper declarations are one of the main tools that Regulated Financial Institutions use to operationalise the Guidelines. Most Regulated Financial Institutions require staff to submit a Fit and Proper declaration upon:

- commencement of employment,

- to reaffirm their status annually, and

- to notify compliance or management when there are any changes in circumstances.

These declarations support regulatory notifications, internal governance and audit readiness. They also serve a simpler but important purpose. They create a structured moment for Regulated Financial Institutions to consider whether anything relevant has changed.

Annual Review as a Governance Practice

Although MAS does not prescribe a single universal annual declaration format across all licence types, annual reaffirmations for Board Members, CEOs, appointed representatives and key appointment holders are widely recognised as good governance practice, ensuring that information on relevant personnel remain updated at all times. This in turn allows for the Regulated Financial Institution to easily demonstrate oversight and governance with the supporting documentary evidence.

As Regulated Financial Institutions approach the new year, these annual reviews provide a natural opportunity to reassess whether existing processes remain fit for purpose, based on the entity’s size, complexity and specific arrangements of its personnel.

Additionally, while frequency may be a contentious point – the market is gradually moving toward conducting more regular background checks as independent, corroborative evidence that regulated personnel remain “Fit and Proper”.

Common Compliance Challenges

Despite clear regulatory guidance, familiar challenges continue to arise across the industry:

- declarations treated as routine formalities rather than substantive reviews

- inconsistent assessment standards across business units

- inadequate documentation to support regulatory notifications

- over-reliance on criminal record checks without contextual analysis

- unclear escalation processes when disclosures are made

Addressing these issues requires more than updated forms. It requires a framework that is understood, applied consistently and supported by governance.

Building a Robust Fit and Proper Framework for 2026

A workable framework does not need to be complex, but it does need to be deliberate.

Key elements should include:

- clear internal policies aligned with regulatory expectations

- structured assessment and escalation processes

- documentation standards that can withstand regulatory scrutiny

- integration with hiring, onboarding and annual declaration processes

- training for HR, compliance and senior management

The Guidelines and their impositions should be treated as a living obligation, embedded into governance rather than confined to periodic compliance checklists.

Conclusion: Understanding Fit and Proper Truly

The Fit and Proper requirements are not a procedural requirement to be completed once a year. It is a governance obligation that reflects a Regulated Financial Institution’s commitment to integrity, competence and accountability.

MAS expects assessments to be fair, reasoned and defensible, taking into account both regulatory standards and real-world context. As regulatory expectations continue to evolve across capital markets and payment services, institutions must ensure that their fit and proper processes evolve accordingly. Doing so protects regulatory standing, organisational resilience and trust.

How Curia Regis Can Support

Curia Regis works with Regulated Financial Institutions in Singapore across the capital markets space as well as payment services, including at the intersection between the two.

Our work supports institutions in translating MAS’ Fit and Proper expectations into practical, defensible compliance frameworks, including:

- Reviewing fit and proper policies and procedures

- Supporting assessments for senior management and representatives

- Aligning internal practices with MAS Guidelines and regulatory requirements

- Conducting governance readiness reviews

- Advising on complex or sensitive fit and proper assessments where judgment and documentation are critical

Ready to strengthen your fit and proper framework for 2026? Contact us to discuss how we can support your institution’s compliance readiness, or schedule a consultation to review your current processes.

You can reach us here or email admin@thecuriaregis.com to get in touch.